Whether your tour and activities company is new to online bookings or well-established, it’s a good idea to keep up with the state of digital payments. In a landscape that’s always changing, it’s easy to get lost or be led astray.

Fortunately, the landscape hasn’t shifted as much as you might think. Despite constant excitement about disruptive payment technologies like cryptocurrency, digital payments have generally gotten simpler over time. Here are some of today’s main contenders:

Payment Gateways

In 2018, tour and activity customers want to book online — and mostly, they want to pay with plastic. They may not be as futuristic as cryptocurrencies or mobile payments, but good, old-fashioned payment gateways are still the best way to take credit card payments online.

But where getting a merchant account to take online payments was once a major hassle, it’s become easier and easier over time. Banks were once the only option, and most had (and still have) aggressive restrictions on what sort of businesses could open merchant accounts. If you were too small or your sales volume didn’t meet an arbitrary standard, it was impossible to get approved. Thankfully, online-only options like Stripe have appeared on the scene, opening online payments up to people and businesses in more regions around the world.

Today, it’s easier than ever to start taking payments online.

PayPal

Once, PayPal was seen as a stepping stone for online merchants of all sizes. When a company first entered the world of ecommerce, building a website that was PCI compliant — that is, compliant with the many security regulations required to take online payments — was often out of reach. Since PayPal handles payment processing on its own website and servers, no special security measures were required. This made it a favorite for many companies first experimenting with ecommerce.

Today, major corporations spend so much on online security that the cost of a PCI compliant website is comparatively negligible. Global cybersecurity is expected to hit $93 billion in 2018, according to Gartner, Inc. Securing a website for online payments is one small part of that massive security market.

Meanwhile, smaller companies take their business to trustworthy services like Rezgo, Shopify, Etsy and others. Those services take care of issues like payment security, so small providers don’t have to go broke setting up online shops. DIY e-commerce sites are no longer as popular as they once were, so alternative payment solutions like PayPal aren’t quite as necessary.

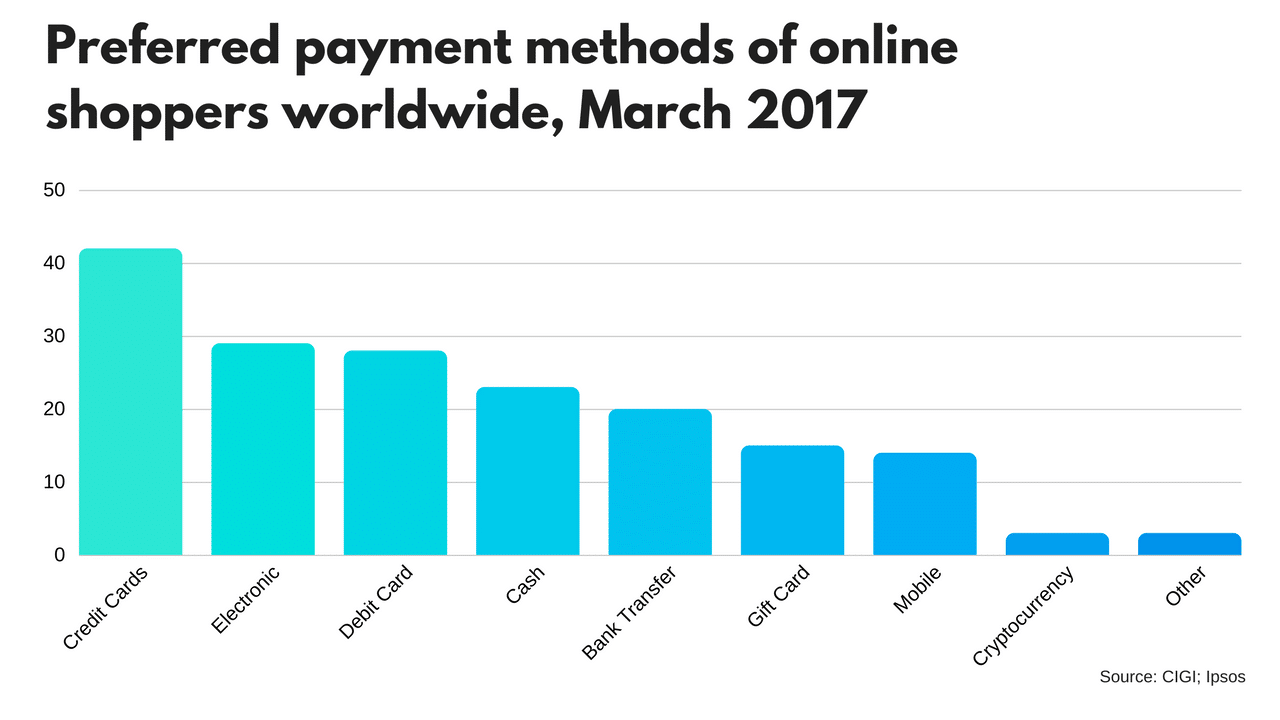

In 2017, credit cards or debit cards were a preferred method of payment for 70 percent of online shoppers worldwide, compared to 39 percent who preferred electronic payments like PayPal (CGI-IPSOS). That’s not to say PayPal is struggling — it’s still a market leader. But in regions where payment gateways are readily available, PayPal is no longer quite as necessary. Not even for small tour and activity companies that are just starting up with online bookings and payments.

Cryptocurrency

While the media frenzy surrounding Bitcoin and other cryptocurrencies might suggest that everyone’s using them for digital payments, the truth is a little less exciting. Only 3 percent of online shoppers prefer Bitcoin as a payment type, and a fairly limited number of merchants accept Bitcoin at all. In fact, the decreasingly enthusiastic response to Bitcoin from both merchants and shoppers resulted in Stripe announcing an end to Bitcoin support earlier this year.

Meanwhile, Bitcoin’s trading volumes keep spiking precipitously high as investors and speculators embrace it as an asset. The day may come when some sort of cryptocurrency becomes an online payment standard. At this point, Bitcoin is likely to remain a favorite for investors, while shoppers stick to more traditional payment types.

Mobile Payments

While everyone else is up at night worrying about cryptocurrency, you can get ahead by considering the real future of digital payments. Mobile payments are growing, driven mostly by the Chinese market. Consumers in China spent US $5.5 trillion through mobile payment platforms in 2016, about 50 times more than consumers in America. With 122 million outbound tourists heading overseas from China that same year, the pressure for businesses to accept mobile payments began increasing, fast.

In China, popular mobile payment platforms include WeChat Pay and AliPay. In some cases, merchants use QR codes to direct customers to pay. In others, Near Field Communication (NFC) is used to allow customers to automatically pay at point of sale terminals. The latter is standard in North America, where Apple Pay, Google Wallet and Android Pay dominate. Even PayPal plans to get into the NFC payment business. Some international payment gateways already support mobile payments through EMV terminals, which may allow you to accept them for bookings through platforms like Rezgo.

If your gateway doesn’t support mobile payments, it’s not worth panicking about. Not yet. Currently, only about 14 percent of U.S online sales are completed through mobile payment platforms, and most regions have a long, long way to go before in-person mobile payment penetration even begins to approach numbers like China’s. But when you’re considering what the future might hold for payments, mobile is the trend to watch.

What it all means

The growing number of digital payment options may seem overwhelming, but here’s the silver lining: it’s easier than ever to accept payments online. With Rezgo, it’s as simple as connecting your accounts and letting us do the rest. Simple, right?

Written By | Nissa Campbell

Search The Blog

Categories

Most Popular Articles

- 16 Innovative Tourism Business Ideas and Trends for 2026

- Your Tourism Marketing Mix: the 7 Ps of Travel and Activity Marketing

- How to Get More Direct Bookings: Strategies for Tour Operators

- How to Cultivate Concierge Relationships for Your Tour or Activity Company

- Tour operator KPIs that actually predict growth