For decades, businesses have relied on a few global standards for payments: credit cards, cash, checks and, occasionally, bank transfers of various types. That’s what we had in the analog age, and that’s what we’ve used in the digital age.

Until recently.

Over the past few years, cryptocurrencies like Bitcoin have emerged as new contenders in the field of online payments. And when you change a system that’s been fundamentally unchanged in decades, you’re going to raise a lot of questions. Questions like “What’s a cryptocurrency,” and “Do I really need to accept Bitcoin?” to start.

What is Cryptocurrency?

First and foremost, cryptocurrencies like Bitcoin, Ethereum and Litecoin are digital assets. They have no real world analogue, no backing in gold or by any government. You can never hold a Bitcoin, or go to the bank and withdraw it directly. That doesn’t mean cryptocurrencies aren’t real. Just as societies agree that this much currency equals that much bread, cryptocurrencies have real value decided by the people who trade in them.

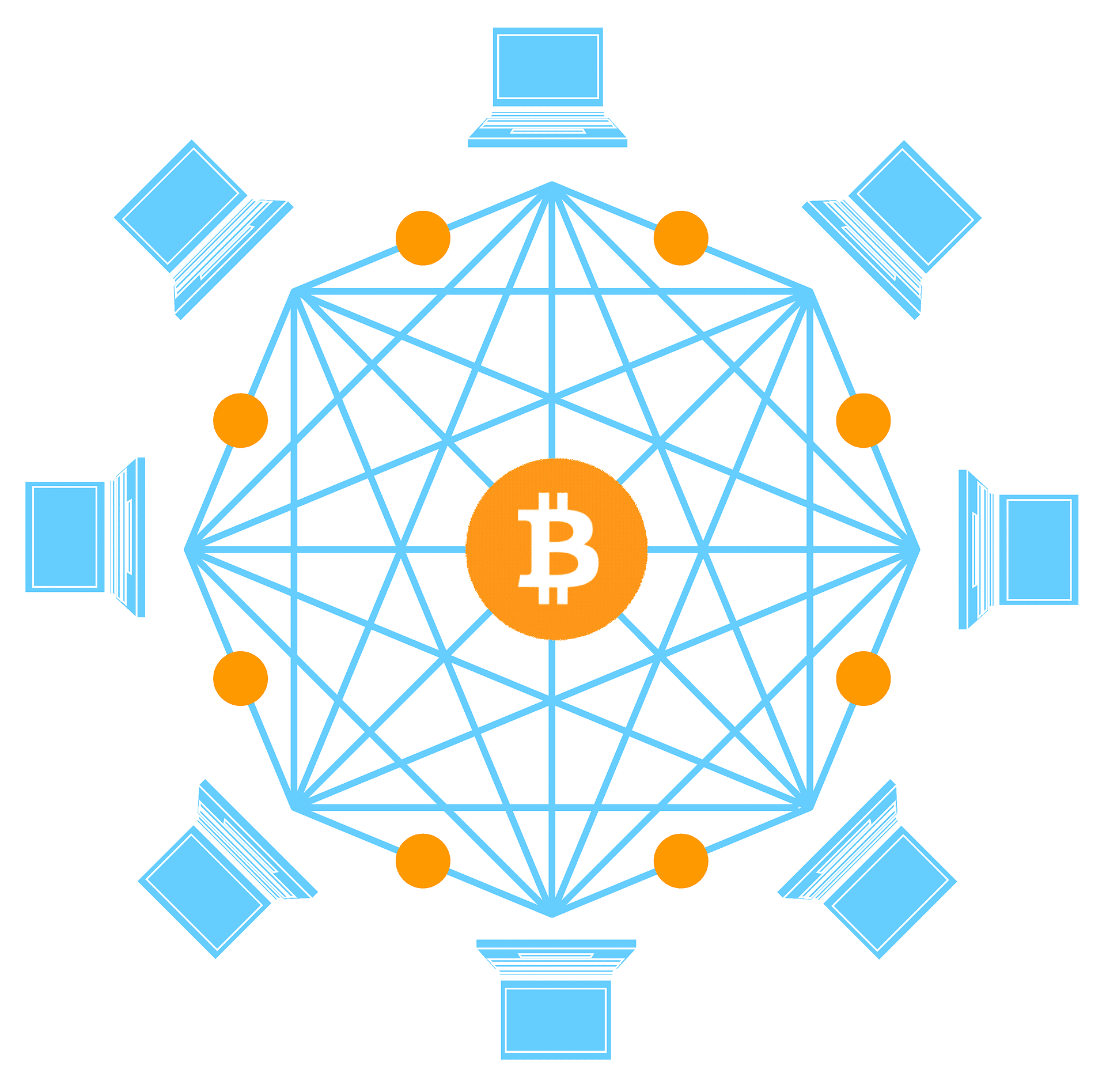

Cryptocurrency coins are generated by computers and entered into a massive distributed network, or public ledger, called the blockchain. The coins can be traded for goods and services at businesses that accept them, or they can be bought and sold with fiat currency (legal tender backed by a government) by investors or speculators.

Beyond their value to speculators, one of benefits of cryptocurrencies is that they can be traded anonymously. This makes them particularly popular in black market transactions and for hackers attacking people with ransomware. For legitimate users, the appeal is often the security offered by blockchain technology.

What’s a Blockchain?

As exciting as the fluctuating prices of cryptocurrencies can be, blockchain technology is where many travel companies are putting their attention. Blockchains are shared public ledgers, distributed networks where a single piece of information — a transaction or smart contract — is spread out to identical, verifiable duplicates on computers around the world. Because the information is stored securely in so many places, it’s virtually impossible to fake or alter, and the information can’t be lost.

To put it another way, let’s consider what goes into buying a house. When you buy a house, you and the seller are exchanging money for property. It’s a basic financial transaction, but because of the complexity and value of the transaction, there are a lot of steps involved. Both sides need to sign a contract and certain conditions need to be met. Large sums of money have to be transferred, and so does ownership of the property.

It’s complicated enough that we bring in intermediaries like notaries and procedures like escrow. They make sure everyone fulfills their responsibilities. They see that the funds and property are both successfully transferred in a way that lets neither side defraud the other. They keep contracts safely stored so they can be verified later. But when you think about it, that process still requires a lot of trust. What if your intermediary loses the contract, or it’s destroyed? What if they’re working with the other party to defraud you? What if they release the funds too soon, and you’re left without the property you bought? Yes, it’s unlikely, but it’s still technically possible.

Blockchains take trust out of the equation, acting as the perfect intermediary. Identical copies of your contract are spread to every computer in the network, each copy verifiable against all the others. The transaction only executes if all its conditions are met. It’s remarkably secure, effectively making several types of fraud impossible.

Where do Cryptocurrencies and Blockchains originate?

To the average user, the origins of cryptocurrencies don’t really matter. If you’re curious, though, cryptocurrency coins are generated, or “mined,” by miners: people who use computers to help automatically process the increasingly large amount of data that the blockchain contains. As a reward for processing their part of the shared public ledger, miners receive transaction fees from users of the blockchain. At the same time, they also help solve complex math problems that generate new blocks for the blockchain. When a new block is generated, the miner gets paid an ever-decreasing bounty of brand-new coins.

The more blocks there are, the harder new ones get to mine, and the lower the reward gets. Eventually, blocks will get so complex that current computers won’t be able to solve the problems that generate them. At that point, no more coins will enter the ecosystem for that cryptocurrency.

Mining is a central part of the cryptocurrency market, but people can trade in cryptocurrencies without having any idea of how it works.

What are the applications for Cryptocurrencies in travel?

The use case for cryptocurrency in travel is straightforward: many people with coins want to spend them, and some businesses see a benefit in accepting them.

Expedia started accepting Bitcoin for hotel bookings in 2014. CheapAir accepts them for flights. H.I.S., a major Japanese travel agency, started accepting Bitcoin in September 2017, and offered promotional bitcoin-only tours to celebrate.

A few smaller companies have also capitalized. For example, Inertia Tours‘ spring break tours can be booked with bitcoin.

For most, the benefit is novelty. Bitcoin owners don’t have all that many places to spend their coins, compared to people using fiat currency, so any company that accepts them is almost guaranteed a captive group of customers. Once, Bitcoin also offered the benefit of quick, inexpensive transactions. Unfortunately, fees have grown with Bitcoin’s popularity, and processing times have slowed dramatically.

What are the applications for Blockchain technology in travel?

While cryptocurrency adoption in travel is on shaky ground, blockchain adoption is exploding. Companies that seem uninterested in embracing the possibilities of a new payment type are finding endless potential in the underlying technology.

Secure, distributed, verifiable data is a powerful temptation for many businesses. With people, companies and even governments losing control of their systems and data thanks to ransomware attacks and other hacks, the protection offered by a blockchain data structure could be invaluable.

But the blockchain isn’t a magic bullet. Several travel companies have pointed to blockchain technology as a way around the issue of distribution. Rather than going through third parties, they can distribute flight or hotel inventory directly to consumers using smart contracts — and that’s true. Both sides could be more flexible, pay fewer fees, and share more data. But distributors like OTAs serve other purposes, like giving consumers a centralized location to find flights, hotels, and other travel products. The success of this shift would require the value of cutting out intermediaries to be higher than the loss of all that visibility, and that remains to be proven.

Beyond decentralization, most applications of the blockchain do their best to eliminate the need for trust. Take vacation packages, for example. The customer needs to trust that airlines, hotels, tour providers and others will all honor their part in the package. The agent who sells the package needs to trust that they’ll receive their commission. The companies involved need to trust that they’ll get the information and payment they expect. Even if it’s all tracked and handled through a central database, one entity owns the database, and everyone needs to trust them. Using blockchain technology, every one of those steps could be tracked, verified, and decentralized. No one needs to place unearned trust in anyone else.

Here are a few more ways blockchains could be used to minimize the need for trust in the travel industry:

Ticketing: Electronic ticketing has its limitations, especially when you work through multiple distributors. Guests arrive with a variety of ticket types, and you need to be able to check them against all the distributors’ databases on the spot. With smart contracts, tickets from a variety of distributors could all tie back to one easily verifiable blockchain.

Identification: Passports are the closet thing we have to a verifiable global standard for identification, and they have limitations. Blockchain proponents imagine a permanent digital identification standard that could instantly be verified against an unhackable, near-indestructible ledger. Of course, this would also require the world to adopt that sort of standard, but there are startups working on that problem already.

Collaboration: Baggage handling, concierge commissions and booking distribution are just a few of the areas in travel where multiple entities have to work together to achieve a common goal — and where better, more trustworthy tracking would be helpful. Smart contracts on a shared blockchain could make it easy for multiple airlines to keep track of each piece of baggage as it makes its way to a destination, or to ensure that everyone receives the correct commission after a referral is complete.

Loyalty: Loyalty programs are often arcane systems that tie dozens of partner programs into a points distribution network that customers can only access under specific circumstances. From onboarding new partners to customer access, a blockchain could make every part of that process more secure and more efficient.

Cryptocurrency has yet to find its place in travel, but giants like Amadeus, TUI, Air New Zealand and Lufthansa are actively investigating the promise of blockchain technology. Beyond them, hundreds of startups are hoping to revolutionize the industry with new blockchain applications.

Today, smaller tour and activity providers probably don’t need to worry much about cryptocurrency or blockchains. Tomorrow, that may change. As the technological landscape shifts, we all need to be prepared to shift with it — and it’s clear we can all expect to hear much more about blockchain-backed travel technology in the months and years to come. Then you can really say… Oh My!

Written By | Nissa Campbell